Agriculture is a risky business - that much is obvious - yet many growers don't regularly assess or plan for risk. This information will help you fill knowledge gaps, so you can effectively manage risks and take advantage of opportunities.

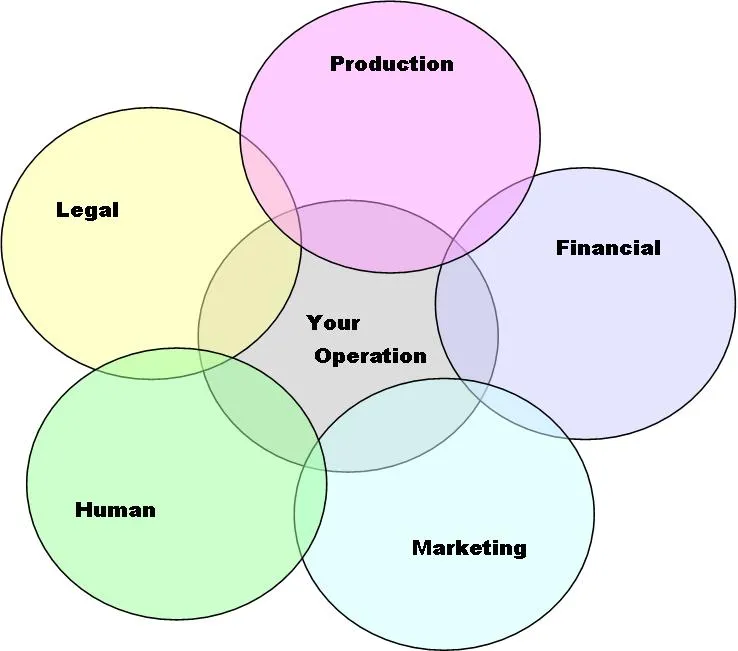

There Are Five Main Types of Agricultural Risk

- Production Risks: Impact production yield or quality

- Financial Risks: Impact cash flow, opportunities for expansion, estate and retirement planning

- Marketing Risks: Impact price and income

- Human Risks: Relate to family, labor resources, and personal health and safety

- Legal Risks: Relate to regulatory compliance (including environmental regulations), liability, and farm succession

These risks overlap in many ways. Decisions made in one risk area can impact other parts of your operation.

On this page:

- What is risk and what can you do about it?

- Risks unique to small farms

- Goal setting, Risk tolerance, Farm business planning

What Is Risk?

Risk keeps you from getting to your goals. It doesn’t just come from obvious sources, like pests, bad weather, market fluctuations, and equipment breakdown.

It also comes from physical incapacitation, from stress and relationship breakdown, and from unexpected liability issues, like letting the neighbor kid come over to pet the sheep.

What Can You Do about Risk?

- Mitigation: You can anticipate unfavorable events and act to reduce the chances that these events will occur.

- Contingency Planning: You also can plan in advance to reduce negative consequences when something bad does happen.

- Standard Operating Procedures: You can create simple guidelines for workers to follow so that each task is done consistently and can be done if you're away.

You will never completely eliminate risk from your operation, and all tools for dealing with risk have some risk of their own.

The question is what are the right tools for you to manage risk and achieve your goals?

Quick Resources:

- Risk Management Checklist - USDA Risk Management Agency

- Introduction to Risk Management - USDA Risk Management Agency

- Don't Break a Leg: Managing Risk on Your Small Farm - Cornell

Click here for more information on general risk management issues.

Small Farms and Risk Management

Small Farms Have Unique Concerns:

- Limited workforce (just family, usually)

- Limited time to study and make decisions

- Limited financial resources

- Difficulty transferring the farm

- Lack of health, disability, and long-term care insurance

- Older equipment and facilities (financial, production, and safety risks)

- Minimize safety risks

- Have a safety manual/training

- Age-appropriate tasks and safety training

- Good agricultural practices

- Foster good-neighbor relationships

- Include neighbors in emergency plans

- Have property, crop, and liability insurance

- Have health and disability insurance

- Have an updated business plan

- Keep good production, marketing, and financial records

- Use consultants, advisors, and free assistance

Source: Joanna Green, Cornell Small Farms Program. "Don't Break a Leg: Managing Risk on Your Small Farm." January 20, 2003

Goal Setting, Risk Tolerance, and Farm Business Planning

Goal setting, knowing your level of risk tolerance, and having a clear business plan are important to managing risk on your operation.

Goal Setting

Be very clear about your goals, so you can figure out what might keep you from reaching them.

Ask yourself:

- Are my goals written, reasonable, and measurable?

- Are these goals attainable in my lifetime? (It's OK if they're not - you just need to include that long-term vision in your planning)

- Have I discussed my goals with my family and employees?

- Have they shared their goals with me?

- Are we on the same page as far as what we want to accomplish and how we want to do it?

Risk Tolerance

Tools for assessing risk tolerance:

- How Risk-Tolerant Are You? - Cornell. Short article and handy checklist.

- Risk and Resilience Assessment - University of Wyoming. Yes/No checklist to assess your operation's level of risk and resilience.

Farm Business Planning

Creating this plan won't happen overnight. It requires a lot of thought, conversation, realism, and research. It also is a "living document": it changes as your goals, circumstances, and needs change.

- Farm Business Plan (OSA 96C) - UCCE Placer/Nevada. All the pieces of a farm business plan

- Farm Business Planning - Oregon State University. Short articles on the importance of a business plan and how to create one.

- Developing a Business Plan - Penn State. Longer article with more detail about putting a strong business plan together.